British American Tobacco – Defining the boundaries of ESG

Successful portfolio management is characterised above all by diversification in order to minimise risks. But how is success measured? At the end of the year, it is measured solely by returns. But how can returns be maximised or risks minimised in the long term while still following ethical principles? ESG investments should make this easier for investors, as all factors are considered here. In the future, regulations of all kinds will oblige companies to comply with certain criteria in order to continue to operate ecologically and economically in the interest of society and, at the same time, to operate in a certain way commercially in order to assure corporate growth.

If one takes a closer look at today's social consensus, equality and equal treatment is one of the most important aspects. Every voice, no matter how abstract, finds recognition and an audience. So, is it justifiable (taking this perspective) to completely exclude entire industries that provide jobs, feed families, and raise taxpayers' money from a projection of the future?

This question is obviously somewhat contradictory when, for example, the tobacco industry is not even considered by most ESG investments. But in an adaptive, ever-changing world through technological advances and new inventions, wouldn't such a move be fatal? Couldn't effective tobacco substitutes stop millions of people from smoking harmful cigarettes and thus save lives?

The contradiction consists of the uncompromising exclusion of several entire industries. By simplifying complex processes, only positive headlines can be created to attract gullible and sometimes unsuspecting investors. Every industry is undergoing a technical change, which means that future ESG investments designed to generate returns must not allow any hasty conclusions to be drawn in order to function effectively. Rationality is required in investing. Biases against certain industries should be re-examined - knowledge is power-.

The 3rd UN Sustainable Development Goal states " good health and well-being". Can a stock like McDonalds count as ESG compliant when obesity significantly reduces life expectancy, strains the heart and leads to organ failure? If investing is seen as investing for the future, the future orientation of tobacco companies would need to be looked at more closely. For decades, no good income portfolio could be imagined without shares in the tobacco industry. The reluctance of ESG investors can be reweighed if these companies are given the same opportunity as, for example, car companies or food manufacturers.

The tobacco company British American Tobacco, for instance, has reduced direct CO2 emissions (Scope 1) compared to the previous year, as well as waste production, energy consumption and water consumption (Source: www.ggx.swiss). So why should a company that is demonstrably taking a step towards sustainability and changing its corporate philosophy to "non-combustible-products" be ignored? The high potential for the investor should receive the same appreciation and information density as other companies that are viewed with an ESG eye.

Tobacco companies have the following characteristics:

- solid revenues and profits

- reliable growth projections

- high dividend yields

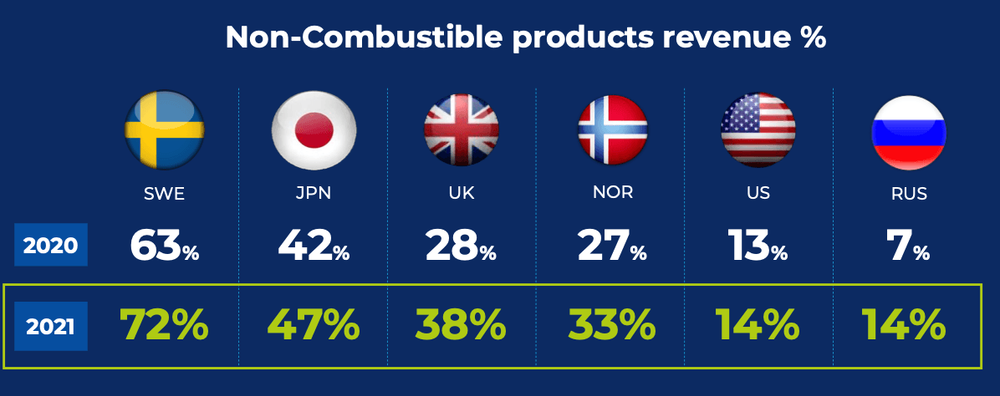

These are all facts that should make even uninformed investors perceptive. The controversy between tobacco and ESG is nevertheless there. To get some facts straight here, take a closer look at the tobacco industry from today's snapshot. People have been consuming tobacco in all forms for thousands of years. The cigarette is just one of many. Could new forms of nicotine use take the place of the cigarette, revolutionising the industry? In the US alone, approximately 31 million people consume cigarettes, and 1600 young people smoke their first cigarette every day (Source: https://www.cdc.gov/tobacco/data_statistics/fact_sheets). These facts will not disappear by excluding tobacco companies from ESG funds. However, investing in the industry will support the shift to more sustainable, less harmful alternatives. E-cigarettes, for example, are significantly less harmful than the conventional product. But e-cigarettes are not the only alternative on the market. NGPs (next-generation products) are gradually replacing cigarettes. These alternatives consist of:

- Vaping: a heating coil heats a liquid to boiling point, which then produces the vapour that the user inhales

- Heated Tobacco: heated tobacco products operate at 250-350°C (cigarettes at around 800). The consumer is exposed to fewer carcinogens and also consumes less nicotine

- Oral nicotine pouches: are not containing any tobacco, only nicotine in crystal form with different flavours

The demand and supply of these products is constantly increasing. So are the revenues of British American Tobacco.

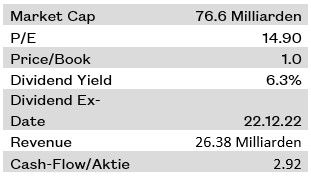

With its strong dividend yield despite a poor economic environment, BAT remains very favourable among investors. The turnover and share buybacks also make the share an interesting investment for the present and the future. The stock market is currently very volatile and turbulent - BAT not. Tech stocks are crashing, value stocks are attracting investors and creating returns.

But can an investment in BAT fit into a portfolio that invests in an ESG-compliant manner?

This question needs to be answered independently... however, it is worth thinking outside the box here. BAT not only delivers strong balance sheet figures and gradually minimises environmentally damaging aspects such as CO2 emissions and water consumption. The business model is designed to provide alternatives to the tobacco industry market today and in the future. Moreover, the timing is suitable. There is a dividend coming this year, UK equities have fallen in value recently and the new Prime Minister should act in the best interests of the financial markets given his economic experience and direction.

In summary, ESG investors should weigh up individually to what extent certain industries belong in a portfolio or not. However, it is important to form one's own informed opinion and not to make sweeping conclusions based on a lack of information.

About the author

Jakob Beckmann is an Associate at Global Green Xchange and Head of the Data Acquisition Team. As one of the authors of the newsletter "Green Money" and of ESG Insights, he regularly analyzes and reports on investment topics and current developments relevant for trading & investing.