GGX ESG Rating - Optimisation of the previous rating by 2 decisive factors

In 2023, we expanded our GGX ESG rating from 15 to 17 factors. Why did this expansion take place? To what extent did we optimise our rating to a new standard?

GGX has deliberately opted for a pure play approach in the selection of ESG factors. The advantage of the GGX ESG rating is that with only 17 factors, all changes in individual indicators are clearly visible and thus the ESG dynamics of a company can be measured transparently and efficiently for the investor - also rationally derived from research and various applications.

Why was the GGX ESG rating expanded from 15 to 17 data points?

Because our aim is perfection and we want to constantly optimise ourselves, we have added 2 rating factors which represent a kind of defence mechanism to identify valuable companies as such.

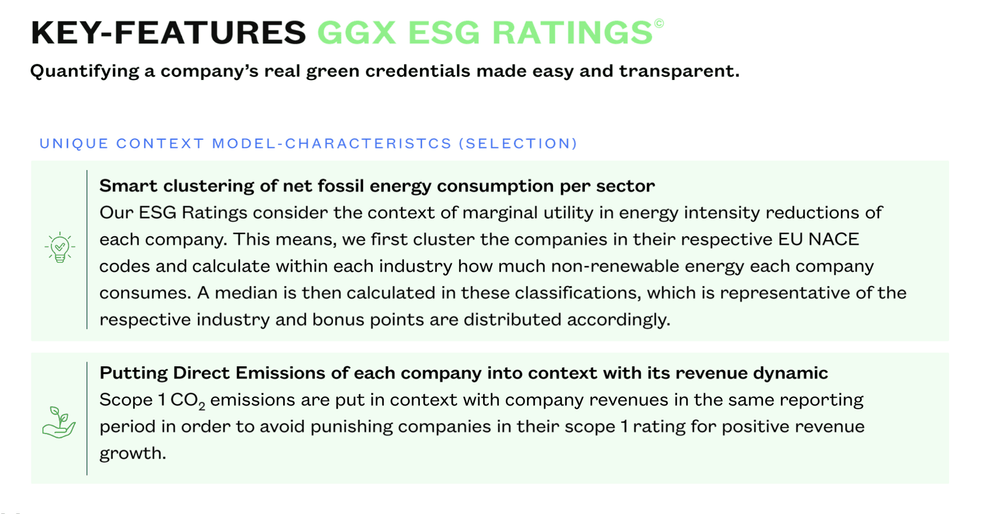

A current problem in ESG ratings is that companies that cause higher emissions receive a poor rating and are therefore not considered for indices or as an investment basis for ESG_investors - this definitely cannot and should not be generalised, as companies that grow exponentially (employees, buildings, trucks etc.) logically also cause more emissions. Portfolio managers, asset managers and investors want returns and the best possible companies in their index (whether ESG-focused or otherwise). To avoid "penalising" companies that operate sustainably and therefore cause higher emissions, GGX has added Revenue as a growth indicator.

If a company increases its Scope 1 emissions and the revenue also increases, the revenue compensates for the points not given.

If a company reduces scope 1 emissions and increases revenue, this is all the more positive for their ESG rating. Vice versa, scope 1 value higher and revenue lower - of course, the worse, as growth in emissions and decline in revenue, are not desirable.

Furthermore, due to the decreasing marginal utility in the delta calculation of energy consumption (companies will not constantly reduce energy consumption by 20% for the next 5 years, as they would otherwise no longer be economically efficient), we decided to classify the companies into their respective EU NACE codes and respectively calculate a median of the fossil energy value for each NACE code (Total Energy Consumption - Renewable Energy Consumption). Based on this median, companies receive additive points. No points are deducted if the value of a company is above the median of the sector.

This means that companies whose energy consumption is below the industry average receive an additive (bonus/reward). This value is not calibrated, but added.

What are the extended 2 data points?

Direct Scope 1 CO2 emissions to company revenue Dynamic factor

Lead factor Additive for fossil fuel consumption

About the author

CMO / Head of Communication & Partnerships der Global Green Xchange AG